Deep Impact: Global M&A plummets in 2H22

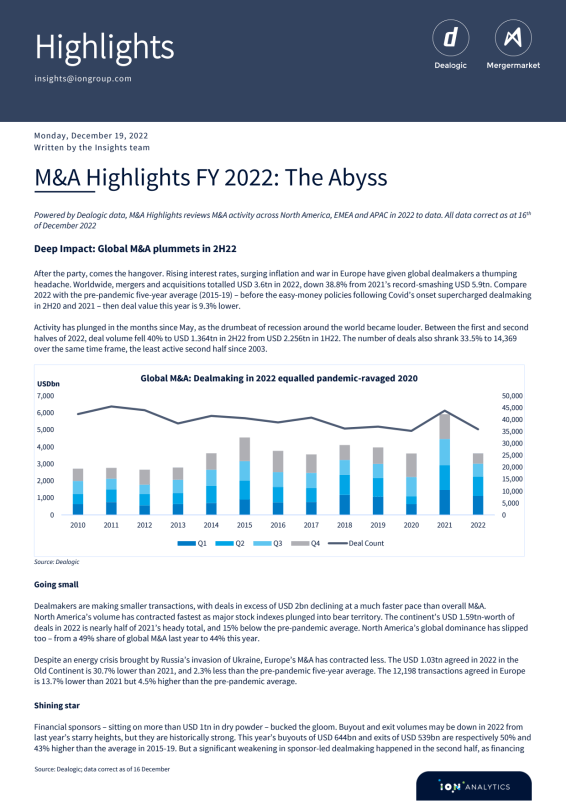

After the party, comes the hangover. Rising interest rates, surging inflation and war in Europe have given global dealmakers a thumping headache. Worldwide, mergers and acquisitions totalled USD 3.6trn in 2022, down 38.8% from 2021’s record-smashing USD 5.9trn. Compare 2022 with the pre-pandemic five-year average (2015-19) – before the easy-money policies following Covid’s onset supercharged dealmaking in 2H20 and 2021 – then deal value this year is 9.3% lower.

Activity has plunged in the months since May, as the drumbeat of recession around the world became louder. Between the first and second halves of 2022, deal volume fell 40% to USD 1.364trn in 2H22 from USD 2.256trn in 1H22. The number of deals also shrank 33.5% to 14,369 over the same time frame, the least active second half since 2003.

Going small

Dealmakers are making smaller transactions, with deals in excess of USD 2bn declining at a much faster pace than overall M&A.

North America’s volume has contracted fastest as major stock indexes plunged into bear territory. The continent’s USD 1.59trn-worth of deals in 2022 is nearly half of 2021’s heady total, and 15% below the pre-pandemic average. North America’s global dominance has slipped too – from a 49% share of global M&A last year to 44% this year.

Despite an energy crisis brought by Russia’s invasion of Ukraine, Europe’s M&A has contracted less. The USD 1.03trn agreed in 2022 in the Old Continent is 30.7% lower than 2021, and 2.3% less than the pre-pandemic five-year average. The 12,198 transactions agreed in Europe are 13.7% lower than 2021 but 4.5% higher than the pre-pandemic average.

Shining star

Financial sponsors – sitting on more than USD 1trn in dry powder – bucked the gloom. Buyout and exit volumes may be down in 2022 from last year’s starry heights, but they are historically strong. This year’s buyouts of USD 644bn and exits of USD 539bn are respectively 50% and 43% higher than the average in 2015-19. But a significant weakening in sponsor-led dealmaking happened in the second half, as financing costs soared, institutional loan issuance dried up, and banks largely stopped underwriting deals because of losses on buyouts agreed before markets sank.

Strong start, weak finish

Seven of the year’s top 10 deals all took place in the first half of 2022. Microsoft’s [NASDAQ:MSFT] USD 75bn purchase of Activision Blizzard [NASDAQ:ATVI], announced in January is still the year’s biggest. Six happened in April and May alone, including VMWare’s [NYSE:VMW] USD 71.6bn sale to Broadcom [NASDAQ:AVGO]; India-based Housing Development Finance’s [BOM:500010] USD 60.8bn deal with HDFC Bank [NYSE:HDB]; Italy-based Atlantia’s [BIT:ATL] USD 46.4bn sale to Blackstone [NYSE:BX]; and Elon Musk’s USD 41.3bn buyout of Twitter. The only top 10 deals to take place in 2H22 were Haleon’s [LON:HLN] USD 30.9bn demerger from GlaxoSmithKline [LON:GSK] in July, Horizon Therapeutics’ [NASDAQ:HZNP] USD 28.3bn purchase by Amgen [NASDAQ:AMGN] in December, and Albertson’s [NYSE:ACI] USD 24.8bn acquisition by Kroger [NYSE:KR] in October.

To brighter days…

Going forward, bankers say there is ample private-equity dry powder and cash on corporate balance sheets for dealmaking to rebound in 2023. Many deals have stalled because of a persistent valuation gap, although that is closing. Given weakened valuations, many companies are opting to sell a stake instead of the whole thing.

Potential deals in the US in 2023 could include food additives business Innophos, which is running a sales process, according to Mergermarket. In Europe, UK veterinary group VetPartners and Italian family-owned pharmaceutical company Alfasigma are preparing for 2023 sales, according to Mergermarket. In Asia Pacific, Norway’s Telenor is looking to divest its USD 1bn Pakistan business, while KKR may opt to sell a stake in pub operator Australian Venue Co after considering a full exit.

Global Intelligence heat chart: Most M&A opportunities are in tech, industrials and pharma

Note: The intelligence Heat Chart is based on “companies for sale” tracked by Mergermarket in the last six months. Opportunities are captured according to the dominant geography and sector of the potential target company.

The full report is available to download on your right.

To download please sign in.