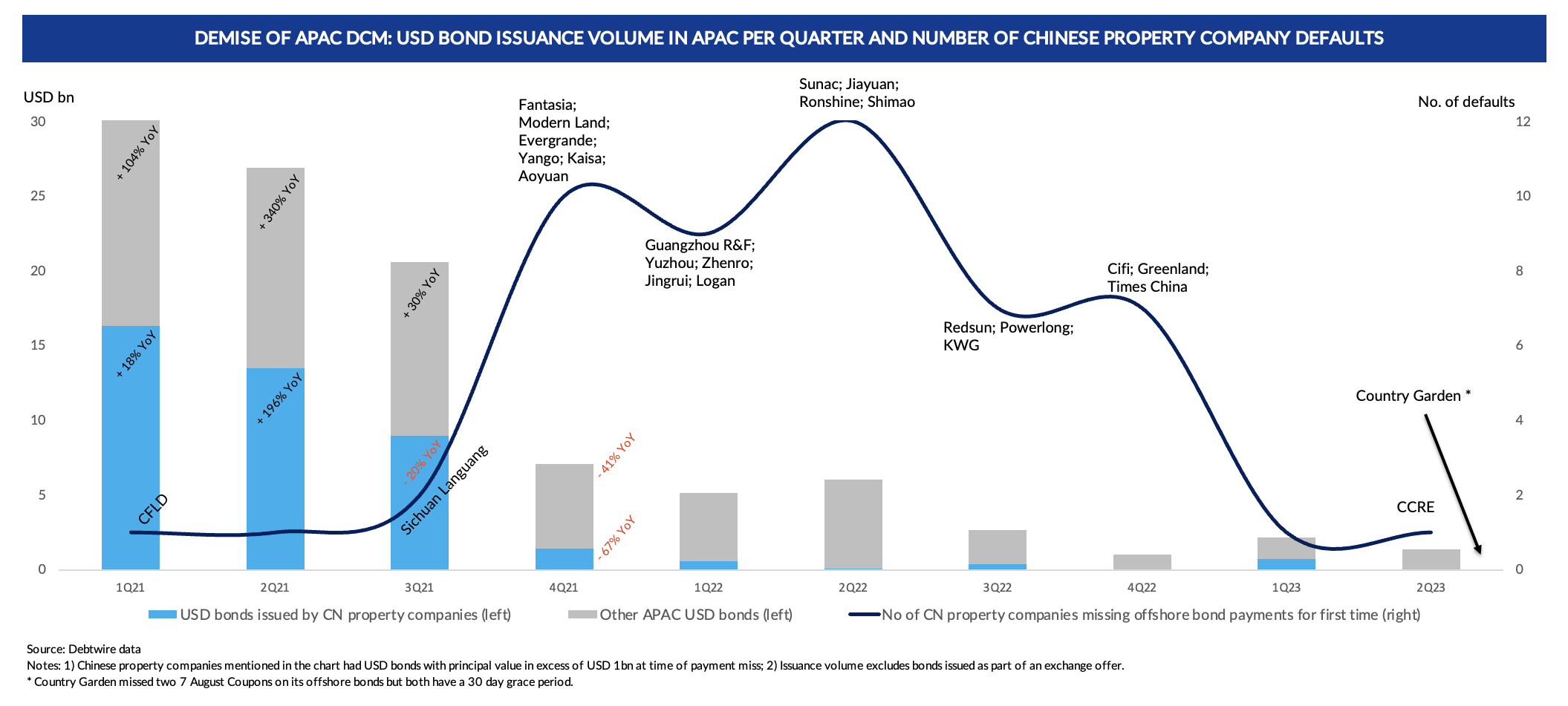

While the issuance of USD high-yield bonds has been lethargic globally since early 2022 amid rising rates, the decline in APAC (ex-Japan) has been very much caused locally, and very much by one specific sector: mainland China property. Conversely, that has been a boon for restructuring advisory work.

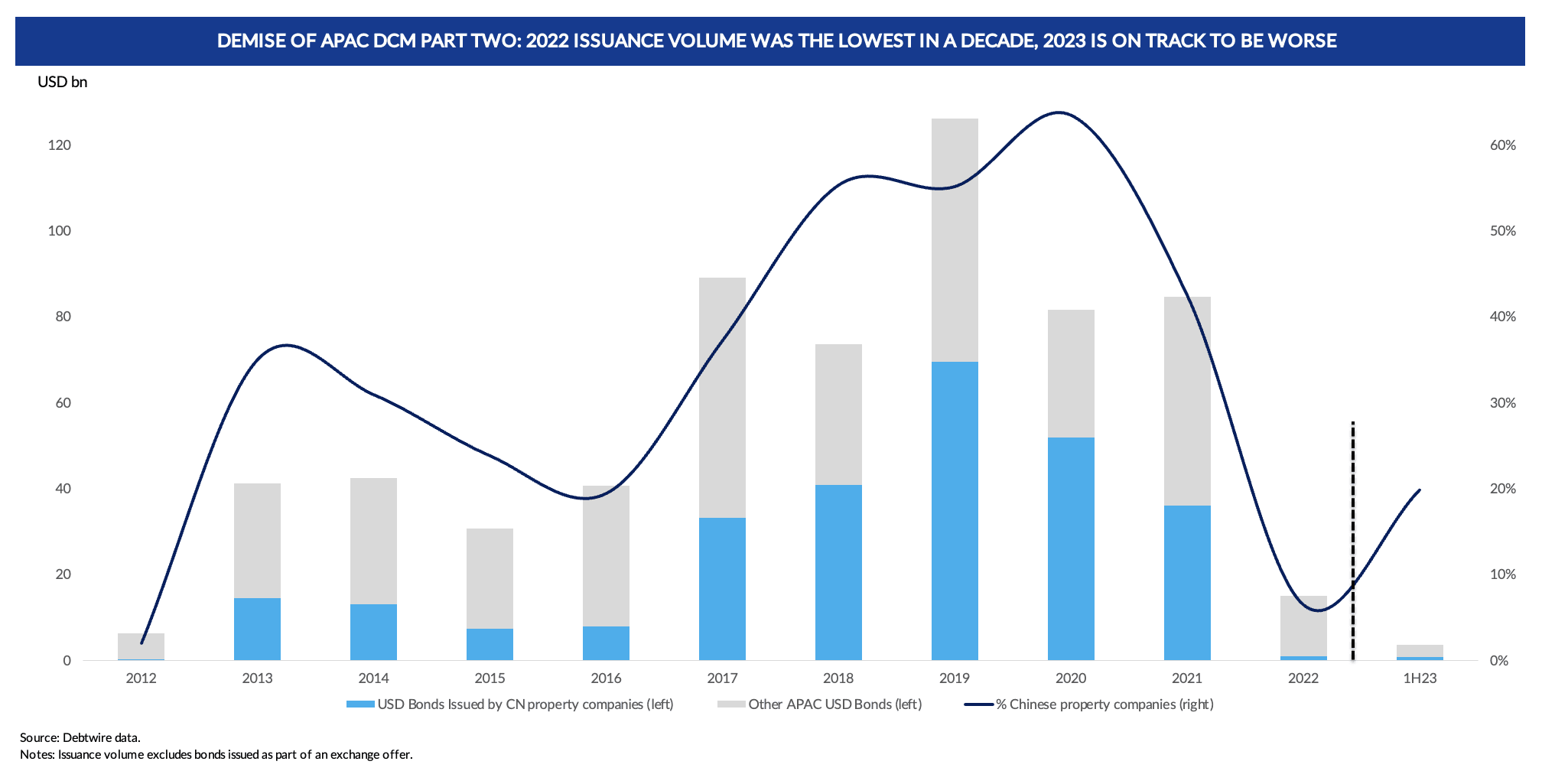

As shown in the table below – powered by Debtwire's Restructuring and Primary Issuance databases – new HY USD issuance volume in the region collapsed in late-2021, just as large Chinese developers began missing payments on their offshore bonds. The sector’s impact on volume has been outsized largely because it has long been the main provider of APAC USD HY bonds.

Surveying the damage

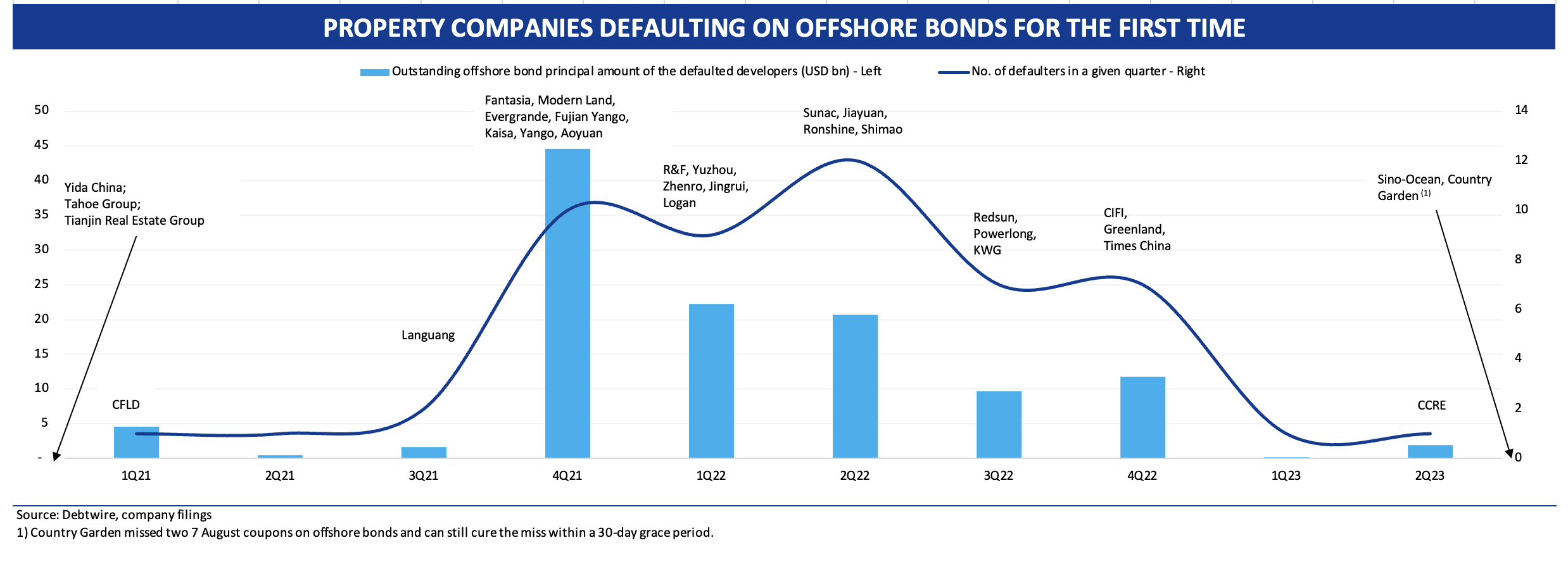

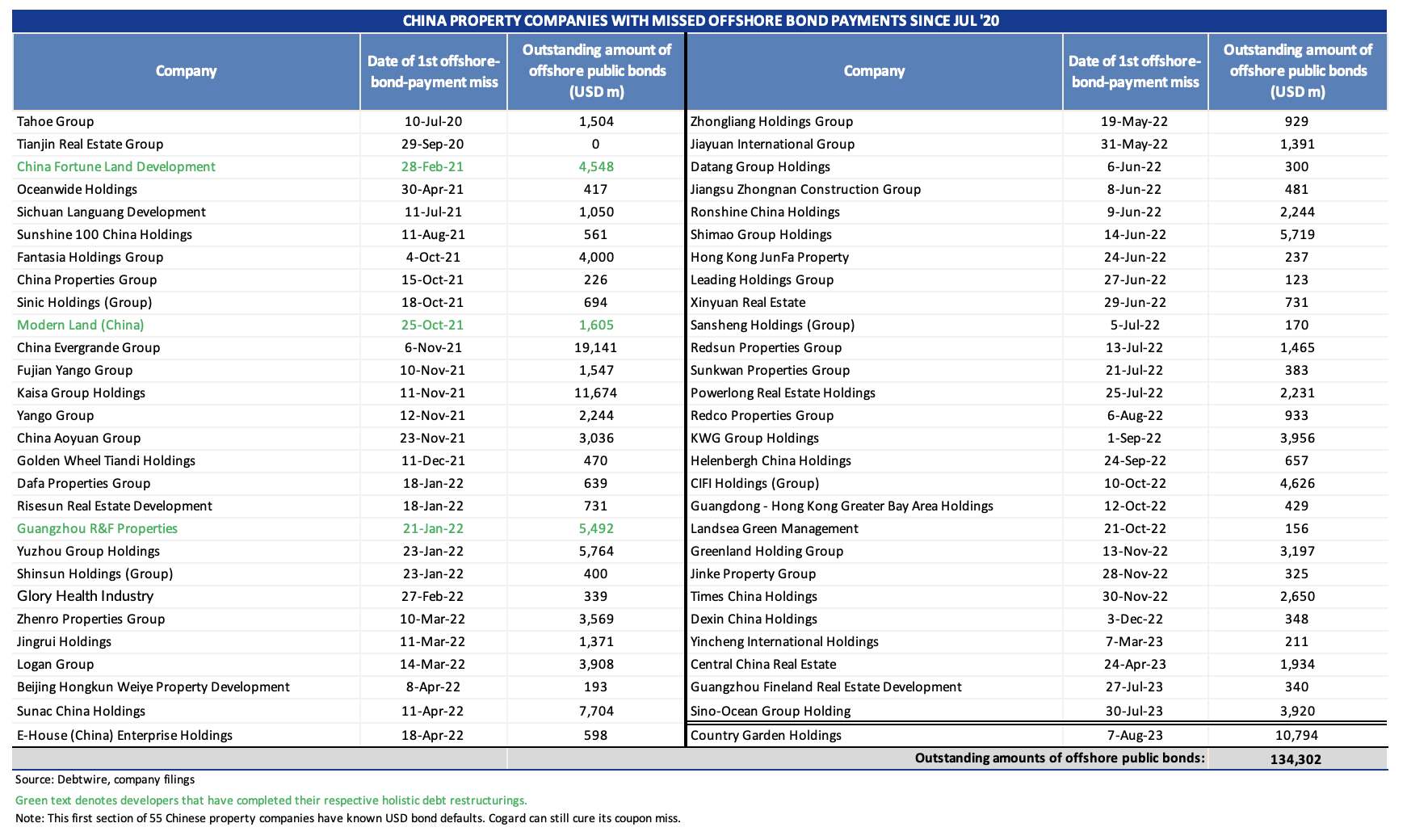

The wave of offshore bond defaults, which formed in mid-2021, crested in the middle of 2022 and has yet to recede. So far, 53 Chinese property companies have been subsumed in the surge, and behemoth homebuilder Country Garden Holdings will be the 54th if it doesn’t cure two missed 7 August bond coupons by the end of a 30-day grace period.

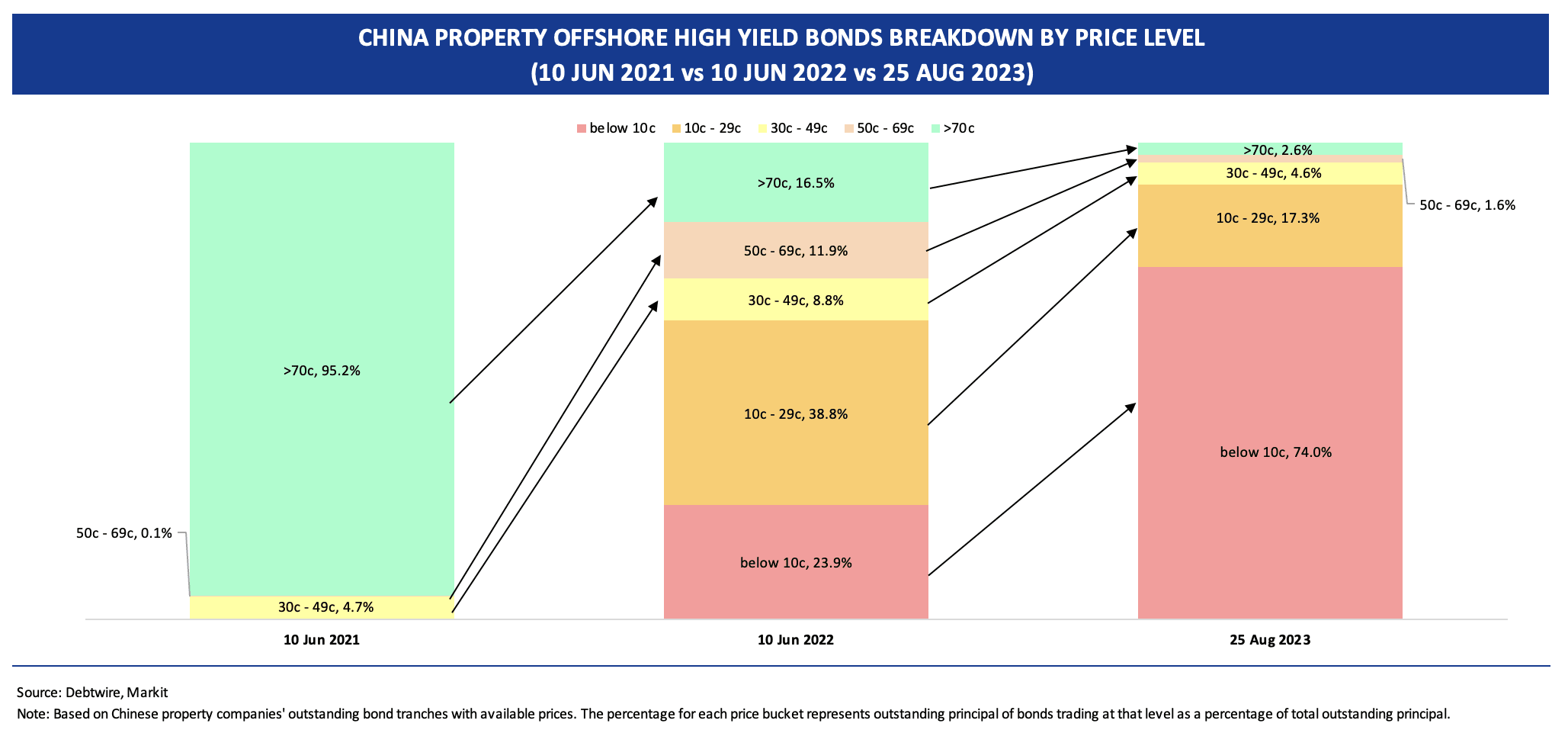

This has dried up demand for Chinese property bonds. Debtwire data shows that non-investment grade Chinese property companies currently have 397 offshore public bonds outstanding with aggregate principal value of USD 154.9bn. They have so far lost more than USD 135.5bn of their market value mostly in the past two years. That is based on 25 August prices from IHS Markit, which covers 367 (includes three CNH and five HKD-denominated tranches) of these tranches with USD 152.9bn outstanding, and cumulatively marks them at a total value of only USD 17.3bn – or 11.3% of the principal outstanding.

Dollar bond issuance dries up

The unprecedented distress in the Chinese property sector has eliminated the key pillar of the USD bond market in APAC (see chart above). For the six months ended June 2023, only USD 3.5bn high yield bonds were issued in APAC, of which one tranche was from a China property developer – Seazen Group's May issuance of a USD 100m due-2024 bond. Overall, the region’s USD high yield issuance in 2023 is on pace to be even lower than a disastrous 2022, which had the lowest annual issuance volume in a decade.

The issuance of APAC (ex-Japan) USD HY bonds had increased significantly, if bumpily, throughout the 2010s, and peaked in 2019, when more than USD 120bn was priced. The growth from 2017 was powered predominantly by the Chinese property sector; it contributed USD 69bn in 2019 or 55% of the total APAC figure, up from USD 7bn/19% in 2016.

Prelude to the tempest

The sector’s offshore bond issuance spree was part of its debt-raising binge that eventually prompted the central government to force developers to deleverage. It was this policy push – not the underlying property market – that triggered the tsunami of defaults.

Indeed, after a sharp but short slump during the early days of COVID-19, contracted sales among high-yield bond-issuing Chinese property developers staged a furious rally.

Data in Debtwire’s monthly China Property Pre-sales Tracker shows that, in 2020, there was a 10.9% YoY increase in aggregate contracted sales by the 53 high yield bond issuing developers that reported comparative figures for that year. Then the 52 developers with comparative data for 1H21 reported an aggregate 34.6% YoY increase for that half. Contracted sales only began to fall sharply in 2H21 and have continued to plummet since then.

Restructuring advisor opportunities

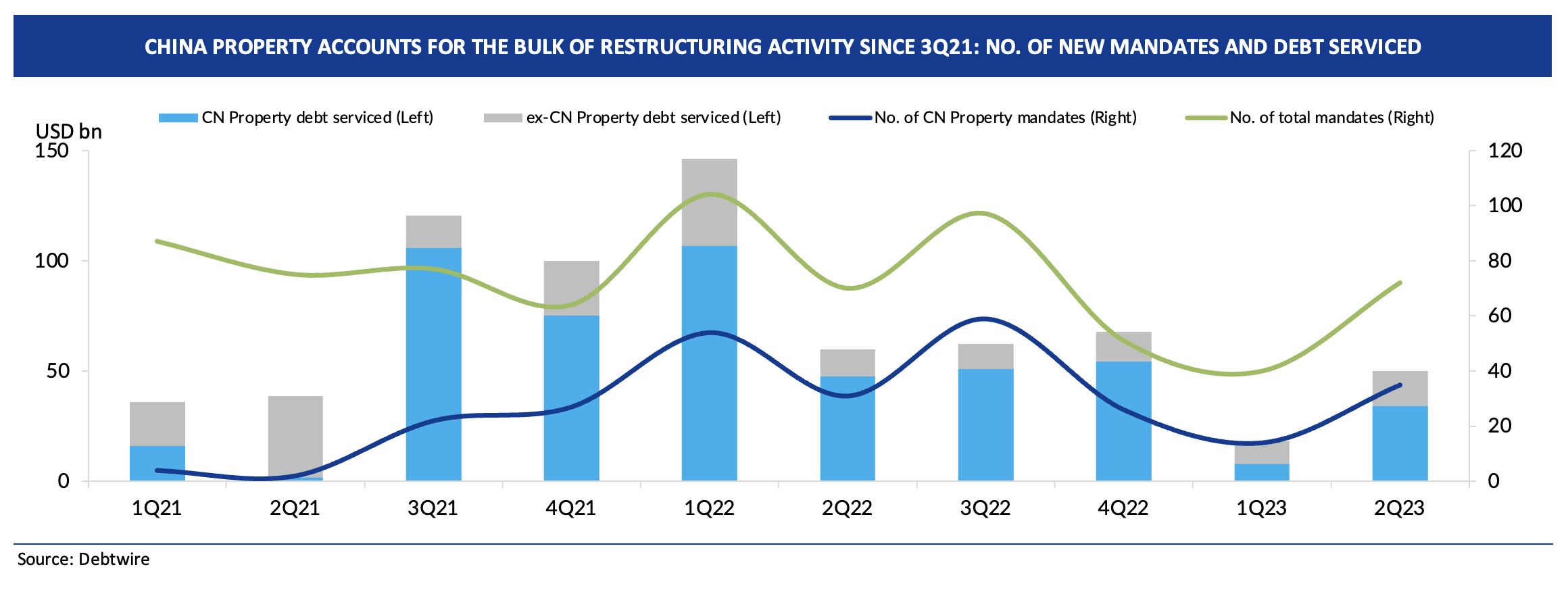

While the carnage in the Chinese property sector has left homes unfinished, and DCM bankers with little to do, it's been a boon for restructuring professionals in the region. As the chart below shows, Chinese property companies have accounted for the vast majority of new restructurings in APAC since 3Q21, as measured by debt amount.

While the total number of new mandates for restructurings involving Chinese property companies has come down in the last few quarters, the sector remains a bountiful source of advisory fees – and headaches. As the chart below shows, 22 Chinese property companies that are currently engaged in a workout process appointed advisors more than one year ago, while another eight are beyond the six-month mark.

Completed Restructurings

Since the current property downturn began in July 2021, 31 developers have completed 39 restructuring processes covering 101 offshore-bond tranches with USD 32.2bn principal (see table below).

Biggest Winners

Four financial advisors – Haitong International, Alvarez & Marsal, Admiralty Harbour and Guotai Junan International – have each received 10 or more restructuring advisory mandates by Chinese property companies or their stakeholders since the start of 2021.

Among international law firms, Sidley Austin leads the pack, with 30 appointments, followed by Linklaters, with 18. Both parlayed their dominance in advising on HY issuance in the region.

[Editor's note – The table in the last section of this report has been changed to reflect that certain restructuring advisors had fewer mandates than originally reported. The changes don't affect the ranking of the top six financials advisors or the top four international legal counsels. The text in the last section has been changed to reflect that Sidley Austin has 30 mandates not 32, Linklaters has 18 mandates not 21 and Guotai Junan has 10 mandates not more than 10.]