Global Overview: Annus Horribilis

What a difference a year makes. At the end of 2021, global equity capital markets looked back on twelve months of plenty. In comparison, 2022 has been a year of famine.

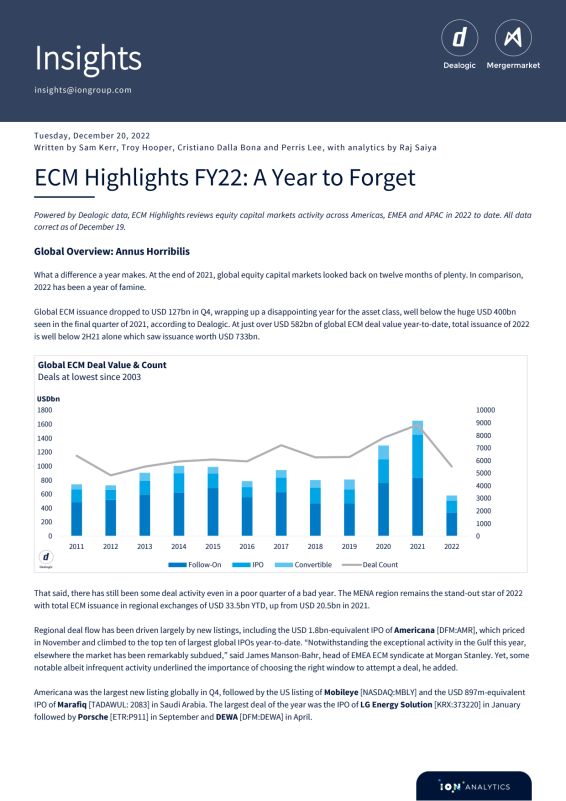

Global ECM issuance dropped to USD 127bn in Q4, wrapping up a disappointing year for the asset class, well below the huge USD 400bn seen in the final quarter of 2021, according to Dealogic. At just over USD 582bn of global ECM deal value year-to-date, total issuance of 2022 is well below 2H21 alone which saw issuance worth USD 733bn.

That said, there has still been some deal activity even in a poor quarter of a bad year. The MENA region remains the stand-out star of 2022 with total ECM issuance in regional exchanges of USD 33.5bn YTD, up from USD 20.5bn in 2021.

Regional deal flow has been driven largely by new listings, including the USD 1.8bn-equivalent IPO of Americana [DFM:AMR], which priced in November and climbed to the top ten of largest global IPOs year-to-date. “Notwithstanding the exceptional activity in the Gulf this year, elsewhere the market has been remarkably subdued,” said James Manson-Bahr, head of EMEA ECM syndicate at Morgan Stanley. Yet, some notable albeit infrequent activity underlined the importance of choosing the right window to attempt a deal, he added.

Americana was the largest new listing globally in Q4, followed by the US listing of Mobileye [NASDAQ:MBLY] and the USD 897m-equivalent IPO of Marafiq [TADAWUL: 2083] in Saudi Arabia. The largest deal of the year was the IPO of LG Energy Solution [KRX:373220] in January followed by Porsche [ETR:P911] in September and DEWA [DFM:DEWA] in April.

Equity-linked activity dropped substantially in the Americas and Asia in Q4 when compared with Q3, but EMEA saw USD 3.1bn printed across 13 deals vs USD 1.9bn across 10 deals in Q3.

Total global convertible bond issuance stood at USD 74bn this year, down from USD 197bn in 2021. Global follow-on issuance followed the same trend totalling USD 336bn YTD, miles away from the USD 834.1bn seen in 2021.

Although follow-ons for the quarter were down too, at USD 78.1bn down from USD 83.5bn in Q3 and USD 210.6bn in 4Q21, follow-on activity in EMEA bucked the trend, increasing to USD 22.1bn in Q4 from USD 16.7bn in Q3. A USD 4.3bn capital raise from Credit Suisse [SWX:CSGN] grabbed the headlines and, combined with an uptick in block trades following positive US inflation data, gave European ECM professionals some league table joy at last.

In fact, the last quarter in Europe provided somewhat of a playbook for banks and issuers in utilising market windows to execute new deals. There are hopes that a period of investor engagement in ECM following on from a better-than-expected inflation print in the US will continue into 2023 and that a global rate rising cycle will peak mid-way next year. This would provide greater opportunities for equity capital market deals throughout the year, including for sellers of positions in the blocks market and companies seeking equity capital for balance sheet repair or even market consolidation opportunities.

“Investors are hopeful of a broader recovery accelerating into the second half of next year. This likely means spotty issuance through Q1,” Manson Bahr added. “Then in Q2 we should start to see more notable activity, likely dominated by primary raises. In Q3 we should expect an uptick in IPOs, with tech listings potentially returning by end of 2023.”

The full report is available to download on your right.

To download please sign in.