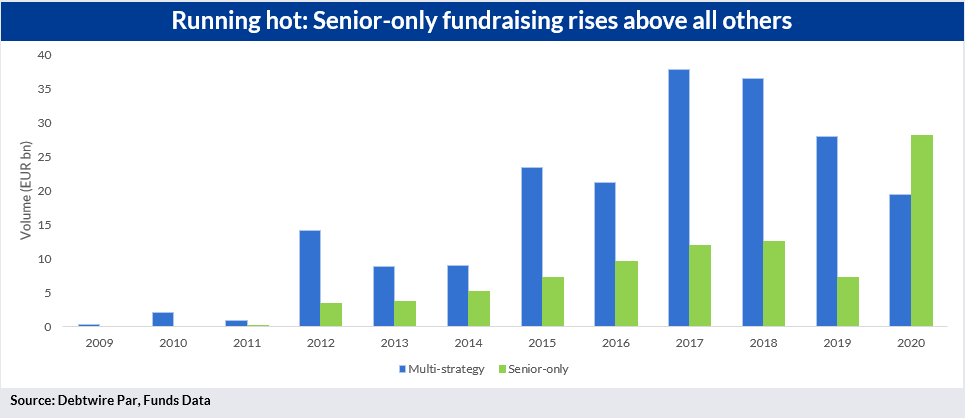

Private debt funds raised solely for the purpose of financing senior facilities soared to EUR 28bn in 2020, having increased progressively since their inception in 2011, and currently stand 135% up versus 2017. By contrast, multi-strategy funds have tumbled since their peak of EUR 38bn in 2017 to reach only EUR 19bn in 2020.

The phenomenon of senior-only funds outpacing all other fundraising activity has only recently been in effect, as can be seen in the chart above. The rise in unitranche activity has contributed to an increase in senior fund demand, with investors starting to overweight first-lien facilities and underweight mezzanine, subordinated debt and equity. This has been exacerbated in 2020, with the greater safety awarded by senior-only facilities coveted by investors in these more uncertain times.

Securing these funds has not been an easy task. Early in the pandemic, fundraisers struggled to secure capital because of a dearth of in-person meetings. However, those firms that have been able to adapt quickly to the new ‘normals’ of Zoom meetings and lower levels of due diligence have thrived.

Opportunities ahead

Over the past decade, unitranche activity has closely tracked senior-only funding levels. As time passes, more and more jumbo unitranches are being raised. This is only possible because of the flood of senior-only funds, which has enabled larger average unitranche deal sizes.

Overall unitranche volumes dipped in 2020; however, this is understandable and in fact quite strong given the circumstances. On the other hand, current unitranche volumes for 2021 are lagging the respective figures from the previous two years.

As restrictions start to lift across the world, fundraising activity should inevitably pick up, as more face-to-face meetings are allowed to take place. This should allow newly-emerging, smaller firms without a track record prior to the pandemic to get a foothold in the market.

Ironically, this may in fact be an opportune time for newer managers to swoop in - incumbent managers will have outstanding funds that have gone through these difficult times, resulting in low returns, therefore nullifying the advantage of a long track record.

There also remain lucrative opportunities for more experienced managers as well. Notoriously more difficult to originate, sponsor-less deals in the form of public-to-private buy-outs are flowing thick and fast following the August break. The wealth of opportunities currently in the market means there is a lot of room to grow for both new and existing fund managers.