Russia’s invasion of Ukraine has given new impetus to biogas, which had already been attracting the interest of infrastructure funds keen to tap into the sector’s role in decarbonisation.

Less than two weeks after the Russian invasion, the EU announced it was doubling its target for production of biomethane to 35 billion cubic metres (bcm) a year within the EU by 2030, as a means to reduce the bloc’s dependence on Russian gas. The new target is more than 10 times the current biogas production of around 3 bcm and a sizeable chunk of the estimated 155 bcm of Russian gas the EU imported in 2021.

The process of increasing production will be assisted by factors such as EU member states having to implement measures for collecting organic waste separately from other rubbish from 2024, the EU said as it announced the target. It also proposed various support measures including using Common Agricultural Policy funds to support farmers in the development of biogas plants.

So far subsidies have largely been enacted at country level and have been necessary because production costs have historically exceeded natural gas prices, although this spread varies in line with gas markets and also has wide geographical variations as data from the International Energy Agency shows.

Soaring energy prices have reduced this gap. On February 17 this year, ahead of the Russian invasion of Ukraine but amid already surging energy markets, the European Biogas Association (EBA) said biomethane can be 30% cheaper than natural gas prices. Nevertheless, government support is needed to scale up the sector in Europe, the EBA said.

Biomethane is biogas, usually produced in an anaerobic digestion (AD) plant from materials such as animal manure that has been stripped of carbon dioxide. Biomethane can be used as a replacement for natural gas in gas grids (with the addition of a small amount of propane), transport and other sectors. Biogas that has not been upgraded to biomethane can be used for functions such as powering heavy machinery.

Biogas can also be produced from organic material that has decomposed on landfill sites although this accounts for a smaller proportion of production than AD plants. The agricultural sector, including manure and other waste material, was the source for the vast majority of new biogas plants installed in Europe last year, according to data from the EBA, with sewage sludge, landfill gas and energy crops accounting for a much smaller proportion. This is in contrast to the early 2010s when energy crops – which are grown specifically to be used for biogas – accounted for the majority or plurality of new plants.

Infrastructure funds that have targeted the biogas sector include Arjun Infrastructure Partners, which acquired a large biogas plant in Denmark from firm Hudson Sustainable Investments and Eurolinque Realty Group in 2020.

“We see biogas as a ‘Cinderella’ sector that has been ignored by investors; to us it’s an important part of the circular economy that reduces the amount of methane going into the atmosphere by using end of life biogenic waste that may otherwise go into landfill (without the methane being collected),” says Arjun Managing Director Nigel Hildyard.

Its contribution to the “circular economy” is also enhanced by the digestate that is left over from the AD process being returned to farmers to be used as fertiliser, he says. Carbon dioxide that has been extracted from biogas to create biomethane can meanwhile be used for making fizzy drinks and other purposes.

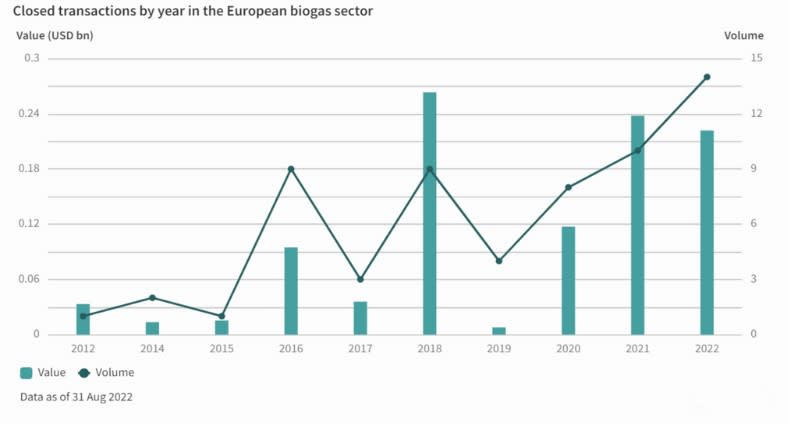

Although biogas has not been completely ignored by investors and investment volumes have been rising in the past decade, it remains a relatively small sector with less than USD 240m (EUR 241m) of investment in Europe in 2021 according to Infralogic data (see chart below). Globally, the sector falls 68th out of 77 subsectors by closed transactions last year, also according to Infralogic data. Those who have entered the sector include France’s Meridiam, which together with local sector specialist Waga Energy owns a portfolio of three AD plants in France.

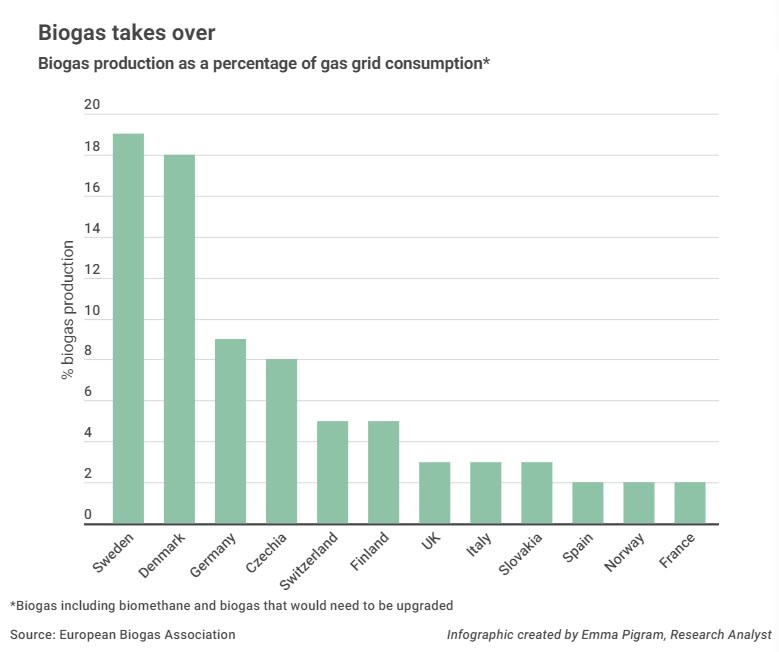

Despite the relative infancy of the sector though, some markets are forging ahead. Figures from the EBA show that by last year, 18% of Denmark’s gas consumption could have been covered by biomethane if all biogas was upgraded, although the country is something of an outlier given its large agricultural sector that largely exports its products such as bacon and butter.

Nevertheless, the European Biogas Association predicts that biomethane could cater for between 30% and 40% of EU gas demand by 2050, compared with 4.6% in 2020.

This will be achieved in part by increased industrialisation of the farm sector. As Michael Ware of the renewable energy financial advisor Green Giraffe notes, meat and dairy production is becoming more intense in Europe, for example with cows being kept in sheds where they produce large amounts of manure that can be efficiently collected and processed.

“This will make AD plants more popular as a means to use the large amounts of waste created,” he says.

However, the sector in Europe may have some way to go to develop the scale needed to attract widespread infrastructure fund interest. Julien Bedin, senior lead for investment research in infrastructure at Partners Group, notes that many of the AD plants in Europe are small facilities processing a limited amount of feedstock, in contrast to the US, where farming is much more industrialised. This lack of scale makes it a challenging sector to invest in, he notes.

However, that could change as the sector develops in Europe. Arjun’s Hildyard said he expects the industry to consolidate, with the many smaller single-farm operations that are in action today being replaced by fewer larger ones that can process a bigger range of material.

Other infrastructure investors to have targeted the sector include Ancala Partners, which in 2018 acquired Biogen, operator of a an anaerobic digestion facility that produces biogas to be converted to electricity.

While pumping biomethane directly into the grid may seem like the most efficient use of biogas, this depends to a large extent on factors such as proximity of the gas grid, notes Nigel Aitchison, head of infrastructure at asset manager Foresight Group. He also notes that AD plants are not an intermittent source of power for electricity unlike wind and solar, which means they can play an important role in securing energy supply. Foresight’s portfolio includes two AD plants in East Anglia that produce electricity.

The extent to which biogas will be used in the gas grid in the future also depends to a large extent on if and when hydrogen will replace methane as the main fuel that is piped though the gas grid for heating homes and in industry.

But such uncertainties aside, the ongoing sale of Nature Energy, a Denmark-based biogas producer that is expanding in Europe and North America, is attracting wide interest despite expectations that the price tag could exceed EUR 1.5bn. Infrastructure investors including Macquarie, Ardian and InfraVia are among those tipped to circle the asset.

One challenge the industry could face as it moves towards larger-scale facilities is securing financing. Paul Winter, whose project management and construction support provider Paul Winter Consulting Ltd. is active in the biogas sector, thinks that government support is needed to bring the sector to a large scale and improve the viability of using new and innovative technologies.

“I think the industry is held back by the investment process; investors are willing to invest in existing facilities with a track record and technology that is proven, but are less keen on newer ones and in particular new technology,” he notes.

Another obstacle is securing contracts that are shielded against energy price fluctuations. While biogas producers can agree power purchase agreements that provide a stable revenue stream, they also need to be guarded against input price volatility, particularly important in the current energy price environment, Winter notes.

Challenges in scaling up the sector aside, unless there is a mass conversion to veganism that deprives biogas plants of manure and other animal waste, one area of certainty in the sector is continuing supply of feedstock.

“The material will always be there, but the issue is cost and how we add value through new and improving technologies in the sector, and these challenges need to be addressed,” says Winter.