Pricing on institutional loans took off in August, rebounding from an historically-tight pricing environment that defined the market at the start of the year. With margins ticking up to 393 basis points (bps), Libor floors ratcheting up to 60bps and original issue discounts (OIDs) rising to 88bps, average loan pricing in August reached its highest level this year at approximately 540bps. By comparison, back in January, when refinancing transactions made up a larger share of issuance (78% versus only 28% in August), pricing had fallen to an average margin of only 338bps, a floor of 24bps and an OID of 46bps.

Thus far in September, average margins and floors have held steady at 394bps and 56bps, respectively, while average discounts have fallen markedly to only 13bps. Given the small sample of loan pricings since the Labour Day holiday in the US, this is largely the product of Weld North Education’s USD 945m TLB repricing at par.

To the fore: As issuance slips, M&A and buy-out share improves

With institutional issuance slowing to USD 43.6bn in August, its lowest level in the year to date (YTD), a steady flow of M&A and buy-out related financings (USD 25.2bn or 58% of monthly issuance) and a slowdown in refinancing transactions (USD 12.2bn or 28% of issuance) contributed to an overall increase in loan pricing. Borrowers looking to finance acquisitions with debt have regularly had to pay a premium.

Wahoo Fitness, for example, issued a USD 225m TLB due 2028 to support its buy-out by Rhone Group. The fitness technology company was forced to widen pricing from talk of Libor+ 525bps-550bps and a 99 OID to L+ 575bps and a 97 OID in order to complete the transaction. Eastman Tire Additives similarly saw pricing flex during the syndication process, with final pricing of L+ 525bps and a 98 OID landing wide of initial talk at L+ 475bps-500bps and a 99 OID. Proceeds support the acquisition of Eastman Chemical Company’s tyre additives business by One Rock Capital Partners.

Of the more than USD 25bn of institutional loans currently in syndication, approximately half are allocated towards M&A and buy-out purposes. Issuers including DexKo Global and PS Logistics are expected to price buy-out related loan financings in the coming days.

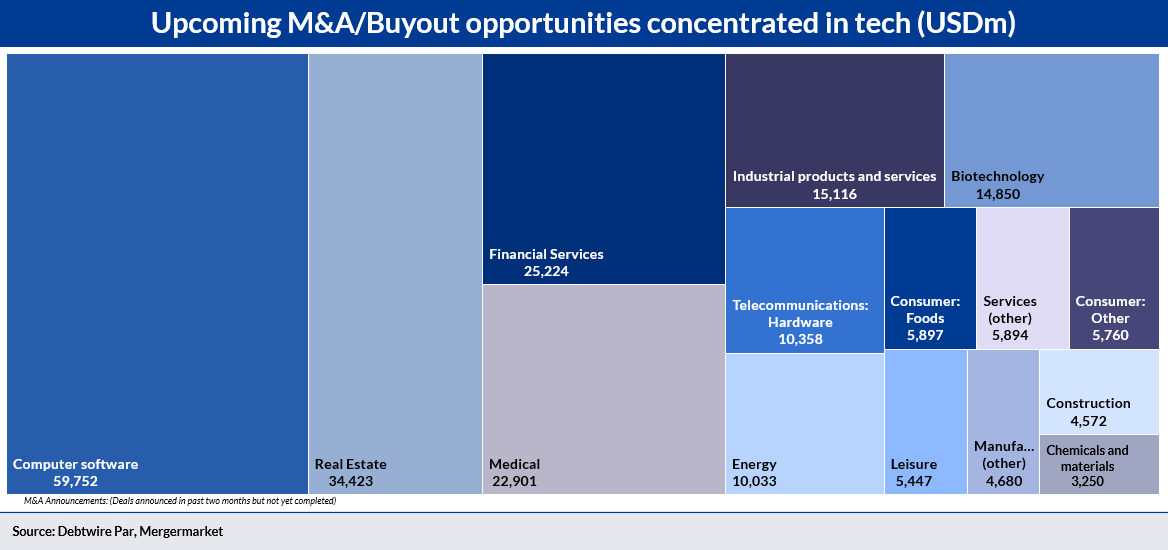

Looking ahead: A healthy pipeline of announced M&A/buy-out situations remains

This is not to say that the late-summer M&A and buy-out boom has reached its end. With around 150 announced M&A deals in the past two months that have yet to complete, opportunities remain to get in on the action. Deals are primarily concentrated in the technology space, with computer software companies accounting for USD 57.8bn of announced deal volumes, followed by real estate, financial services and healthcare companies.

Some of the largest expected deals fall into these sectors, including Hill-Rom’s USD 10.5bn acquisition by Baxter International, Lumen Technologies’ USD 7.5bn sale of its incumbent local-exchange carrier business to Apollo Global Management, and Inovalon’s USD 7.3bn acquisition by a consortium of investors led by Nordic Capital and Insight Partners.