High-yield (HY) bonds are moving into the limelight, having risen to the highest proportion of leveraged capital market debt at over 40% of issuance in 3Q20.

This trend looks set to continue, with bonds such as Wallenius Wilhelmsen’s NOK-denominated senior unsecured note continuing to trickle through the market in August. Meanwhile, loan syndication in Europe is still smarting from the rocky end of issuance prior to the August break.

Decisions, decisions

In many ways, there is little to separate HY bonds and leveraged loans because of a convergence of their documentation in recent years. Covenant-lite loans remain the norm and were even touted as a benefit during the stressed times at the height of the pandemic – allowing firms to ride through tough times without triggering events of default and then enabling them to bounce back when conditions improved.

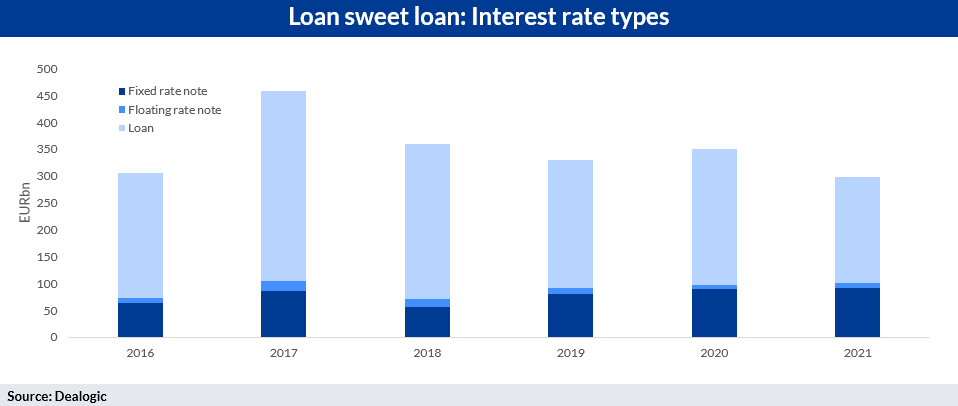

Nevertheless, there remain several differences between the two asset classes. Coupon type is one of the most significant – bonds are predominantly fixed-rate instruments, whereas loans have margins floating over a benchmark. When interest rates are expected to rise, borrowers pivot to bond issuance to maintain low interest expenses.

While floating-rate note (FRN) issuance is significant, these deals have not contributed to the recent rise in bond volumes as a percentage of overall leveraged activity. FRNs have consistently been issued at around 5% of leveraged loan issuance in recent years.

Another prevailing distinction between bonds and loans is call protection. HY bonds usually have non-call provisions for a number of years, preventing the issuer from calling the bond early. This allows for price appreciation beyond par during the non-call period in improving market conditions; however, during poorer market environments, this provision becomes less limiting for borrowers, making bonds more attractive.

Meanwhile, leveraged loans’ standard six-month soft call of 101 means redemption prices stay at or near par during strong market tailwinds, meaning issuers are more likely to lean towards loans during periods of growth.

With expected tapering of quantitative easing and rising interest rates, the fixed-rate nature of bonds should lead to an increasing leveraged market share. Moreover, if current bearish market sentiments play out, call protection will be less of a limitation for issuers - further boosting bond issuance.